Investors have been navigating the uncertain and turbulent waters of Times Trump, where one social media post can send markets soaring, announce a military action or a ceasefire. Our January 2026 edition focused on Trump’s tariffs and their effects on U.S. inflation, the dire trade threat to the Canadian economy and the mortal threat to the global trading regime and its underlying multilateral treaties. The then very recent January 3rd U.S. operation to detain Venezuelan President Maduro seemed to us to encourage President Trump’s aggressive unilateralist and military urges:

“As a triumphal Trump said in his news conference after capturing Maduro: The future will be determined by the ability to protect commerce and territory and resources that are core to national security… These are the iron laws that have always determined global power, and we’re going to keep it that way.”1

Now the financial and energy markets have run aground in the Strait of Hormuz. We and most knowledgeable experts had no idea that the perceived acclaim, ease and success of Trump’s Venezuelan adventure would lure him into trying his hand at Iran again. Our worries about eventual tariff driven inflation now seem quaint compared to what is going on with Iran’s blocking of the Strait of Hormuz and the damage to the oil industry in the Middle East, neither of which seemed considered in potential Iranian responses to the attack by the U.S. and Israeli militaries.

Trump’s so-called Donroe Doctrine was meant to protect commerce and resources as part of his mercantilist America First agenda, but energy markets and commerce don’t end at the U.S. border. The U.S. might produce enough oil for its own needs but, absent a ban on exports or price controls that would enrage U.S. producers, oil and natural gas commodities whose prices are set globally. Higher aviation fuel prices affect American airlines and tourism immediately and eventually aircraft manufacturers like Boeing if global airline traffic drops. The soaring global energy and oil prices question Trump’s braggadocio about a quick and surgical end to his “non-war” with Iran. Unfortunately, high energy prices will weaken U.S. and other global economies and cause inflation at the same time. The question is really for how long and we’re now just in the early innings of this energy disruption.

Victorious Statistics

In an eerie parallel to the Vietnam War “Body Counts” that promoted military success by statistics, President Trump and Peter Hegseth, his Secretary of War, have self-declared their war ended several times, based on their iteration of Iranian military “target packages” destroyed and Iranian leaders “decapitated”. All that unilateral victory aside, it was Trump who seemed to back off on his increasingly apocalyptic threats when he announced a 2-week ceasefire based on an Iranian 10-point plan that was basically an Iranian wish list including retention of enriched nuclear materials, control of the Strait of Hormuz, reparations for war damage, all in return for a complete reopening of the Strait of Hormuz to obviously get energy prices down.

Blockading the Blockade

A “complete reopening” under Iranian control and tolling seemed to us to be an oxymoron. Then Mr. Trump muddied the waters even more by suggesting that the U.S. would participate in that tolling system. Trump then delegated Vice-President Vance to negotiate with the Iranians in Islamabad with the Pakistanis as mediators. With the Islamabad talks based on an Iranian wish list, it is not surprising that Vance announced that the result was “No Deal” after 21 hours when the talks ended. Soon afterwards, 2 U.S. destroyers sailed through the Strait and President Trump announced a complete naval blockade of the Strait and prevention of passage by any ship that has paid a toll to Iran. He also said that the U.S. Navy would begin demining the Strait, adding that “Any Iranian who fires at us, or at peaceful vessels, will be BLOWN TO HELL!” It was soon after announced that the U.S. Navy’s blockade, a specific wartime term under maritime law, would apply to ships transiting in and out of “enemy” Iranian ports and the Strait would be open to free transit. No doubt someone in the Trump Administration recognized the bad precedent that would have been set for the South China Sea!

A Reshaped Battlefield

As we said about the opening salvoes of Trump’s Beautiful Tariff trade war, no war plan survives contact with the enemy. Early triumphs are not determinative of eventual success, as Germany and Japan found out in World War 2. Other U.S. Presidents saw initial military victories fade as things dragged out, along with U.S. confidence and commitment.

We are not military experts, but generals usually “fight the last war”. Most of what we hear in the media from the military commentators about the current Iran war situation is based on the experience of prior wars. “Boots on the Ground” in Iran are not just politically unpopular, they could be very risky for the troops involved. Like the introduction of the machine gun in World War 1 and IEDs in Afghanistan and Iraq, new technologies “reshape the battlefield”. As the Ukraine war shows, drones have altered the calculus of modern ground warfare. The Ukrainians pioneered the use of cheap consumer drones armed with grenades and shells against a larger and better armed enemy. Then they turned to domestic production, improved their drones considerably and altered their military command and control to exploit this new technology.

The Asymmetry of Drone Warfare

Also faced with a large and powerful enemy, the Iranian regime has long invested in asymmetric weapons. Russia has used borrowed Iranian Shahed drone technology in its aerial bombardment of Ukraine. Even the U.S. is said to have used reverse engineered Shahed drones against Iran. The Iranian allied Shia militias have used drones against the U.S. military in Iraq and against the Israeli military in Lebanon. The Houthis in Yemen have used airborne drones of various sizes and destructiveness and sea drones in neighbouring waterways. The Iranians have already used sea drones in the current conflict, as the Wall Street Journal reported:

“The Revolutionary Guard has also begun using waterborne drones to attack ships. The Marshall Islands-flagged Safesea Vishnu tanker was attacked by two explosive-laden drone boats in an Iraqi port on March 11th… The MKD VYOM, a Marshall Islands-flagged oil tanker attacked near Oman, and the Bahamas-flagged crude oil tanker Sonangol Namibe anchored near Iraq’s Khor al Zubair port, were also struck by naval drones… The Revolutionary Guard first displayed its naval drones about a year ago in a video of an underground base. The Iran-backed Houthi militia in Yemen used drones in 2024 against commercial vessels in the Red Sea, the U.S. military said at the time. Security officials said then that the technology behind the remote-controlled drones had been provided by Tehran.”2

As the Russian Navy has found out in the Black Sea, after losing their flagship cruiser and over 20 other ships, sea drones would make an opposed military and naval operation to reopen the Strait of Hormuz very dangerous for conventional naval ships. The lessons of Ukrainian/Russian drone warfare are not lost on other militaries, including the U.S. It has been reported that a war hardened and experienced Ukrainian 10-person drone team decimated a conventionally armed 1,000 soldier North Atlantic Treaty Organization (NATO) battalion in practice war games in Estonia. Given that existing NATO doctrine is largely U.S. military centric, one can see the U.S. reticence for ground operations in Iran. A NATO frigate also suffered a number of sea drone attacks from Ukrainian opposition in a naval war game and was said to have been “destroyed” before the crew even knew they were under attack. While these were just war game exercises, the simulated results parallel the Ukraine war reality of conventional weaponry and tactics meeting drone warfare.

The Largest Energy Shock in History?

Geopolitical and military considerations aside, the real economic and financial question is how long the disruption to the Strait of Hormuz will last and how long will it take to get back to normal energy markets afterwards. The International Energy Agency (IEA) in Paris said in its March Oil Market Report that “the war in the Middle East is creating the largest supply disruption in the history of the global oil market”. Most energy experts believe even if there is a miraculous and immediate reopening to unimpeded ship traffic, it will take some time to restart even the undamaged facilities and obviously longer for those that have been damaged by attacks by both sides.

We suspected that Trump’s tariff strategy would take some time to feed through into U.S. inflation. The recent spike in energy prices is hitting inflation and consumer’s wallets much more quickly. The average U.S. gasoline price per gallon was just under $3 before the attack on Iran and it is now over $4 per gallon, up 33% in a month. That led to a 0.9% increase in the overall U.S. March CPI. Canadian gasoline prices are up a similar 33% and other countries, especially in Asia, are having to ration gasoline and other energy products. They are also allowing remote work and shortened work weeks to deal with reduced energy supply.

The political pressure of higher energy prices seemed to be getting to the President before his surprise ceasefire announcement. His rhetoric on the Strait of Hormuz ranged from: I don’t care; the Strait will open itself; the U.S. Navy will escort ships through; it’s not my problem and culminated in, just before the announced deadline for his threats to destroy Iran’s bridges and power plants with “Open the F…kin’ Strait, you crazy bastards…” That showed his anger and frustration very clearly and was followed up with his threat to completely destroy Iranian civilization.

Oil Uncle

That Trump ultimatum was avoided by the 2-week ceasefire that was to be followed by a permanent agreement. Now that the talks have failed and the Strait still remains closed, Trump’s U.S. counter-blockade is a high stakes game of “Oil Uncle” to see who flinches from the pain first. Trump had previously lifted the embargo on Iranian oil already at sea to lessen the impact on energy prices. Now, in the hope of gaining leverage over Iran, he’s taking all Iranian oil completely out of the system. That threatens to make the IEA’s worst energy disruption in history even worse. The question is who is going to feel the most pain first. Trump knows that the economic impact of his attack on Iran is politically dire for him and the Republicans, but that’s already locked in. Why not just go “all in” and hope for Iran to “cry uncle” first and get to actually declare victory.

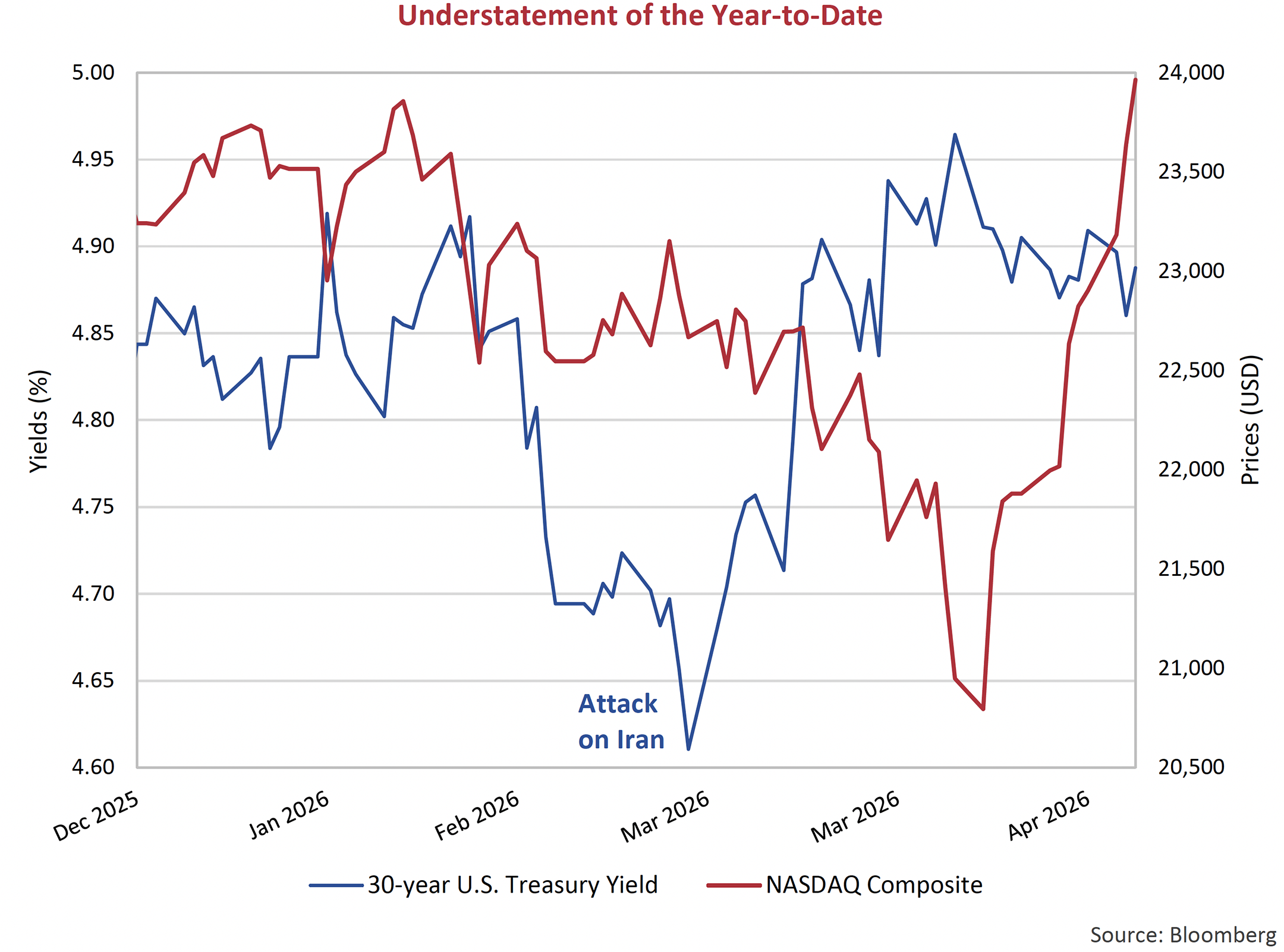

Understated Market Reaction

We don’t know what either Mr. Trump or the Iranian regime will do, but it is interesting to us how understated the stock and bond market reaction has been to the surge in energy prices due to the Iran conflict. The chart below of the 30-year Treasury yield shows it has increased from 4.6% just before the attack on Iran to the current 4.9%, up only 30 basis points (bps) or 0.3% and not too far from where it started the year. That pales compared to the run up in the 30-year yield starting in 2021 when post-pandemic inflation and energy fears over Russian/Ukraine war saw the 30-year yield rise from 3.6% to over 5.0%, up 1.4%.

Bond investors obviously don’t agree with the IEA that this is the largest energy shock in history and see the problem as temporary, given the benign increase in bond yields. The equity markets also aren’t impounding a massive historical disruption to global energy markets and economies. The NASDAQ index level shown in the chart above shows it has recovered all its initial losses after the attack. When markets opened on the Monday after the Islamabad talks ended without a deal and Trump announced his own blockade, bond yields were up only slightly, and stock prices rose. By the end of the day, 30-year Treasuries were down 1 bp, and the S&P 500 equity index rose 1%, also wiping out its loss for 2026. Even oil was up a mere 3% to $98 after reaching $103 when the talks collapsed and now sits at $95. Not what one would expect from the greatest energy disruption of all time! It helped that the ceasefire held and that Trump and his staff let it be known that Iran wanted to continue talking and was “begging for a deal”. Investors are so used to President Trump backing off when he causes market upset that they are more fearful of missing out on the subsequent rally than the damage that higher inflation could do to their portfolios.

The Politics Aren’t So Easy

Investors might not be that worried about the Iran conflict and energy prices, but the U.S. politics aren’t so easy. Voters are experiencing soaring prices that 2024 candidate Trump promised to lower and a foreign war that Trump promised to avoid. Before the attack on Iran, Donald Trump was calling the “Affordability Crisis” a “Democrat Hoax”, despite polls showing that to be the major concern of U.S. voters. With gas prices now at above $4 and the CPI up 0.9% in March, he has his work cut out for his Administration on affordability. Trump now admits that these higher energy prices may not fall any time soon:

“President Trump conceded that energy prices may not fall soon and could be higher around the time U.S. voters head to polls in midterm elections this fall. Asked Sunday on Fox News if he thinks oil and gas will be lower then, Trump said: “I hope so. I mean, I think so. It could be (the same as now) or maybe a little bit higher. It should be around the same…””3

A weakening economy with higher inflation is not where the Trump Republicans want to be just before the coming mid-term elections in October. That seems to be the case, according to the March Institute of Supply Management (ISM) survey:

“U.S. services sector growth slowed in March, while prices paid by businesses for inputs climbed to near a 3-1/2-year high, an early sign that the prolonged war with Iran was boosting inflation pressures… …The ISM survey’s measure of prices paid by businesses for inputs soared to 70.7, the highest reading since October 2022, from 63.0 in February.”” US service sector cools in March; price paid measure highest in 3-1/2 years.”4

2024 candidate Trump unrealistically promised to get prices back to where they were before the pandemic. That hasn’t happened and voters are now seeing a new bout of inflation. The real pain point for voters is affordability, and the higher gas prices they are paying are obviously not a hoax. As higher energy prices exert their effect on other parts of the economy, it will get worse before it gets better. Fruits and vegetables need truck transport to grocery stores and truckers will charge more for transport as their costs go up. Manufactured goods transported by train and ship will have higher costs with diesel and Marine Bunker C fuel more expensive. Air travel and transport have seen that fuel cost increase as well. Even Uber drivers need higher fares to pay for their gas.

Will Inflation Persist?

We agree with the financial markets that inflation will not necessarily be a long-term problem, but that depends on monetary policy and whether central banks will ease policy excessively to offset this “oil shock”. That’s what they did after the 1973 oil shock during another Middle East conflict that ended up with the high inflation 1970s. The initial “Cost Push” inflation from rising oil prices was extended into “Demand Pull” inflation by excess money supply. It took very high interest rates from the Volcker Fed to finally tame that severe inflationary period, at the cost of a severe recession.

Show Us the Money

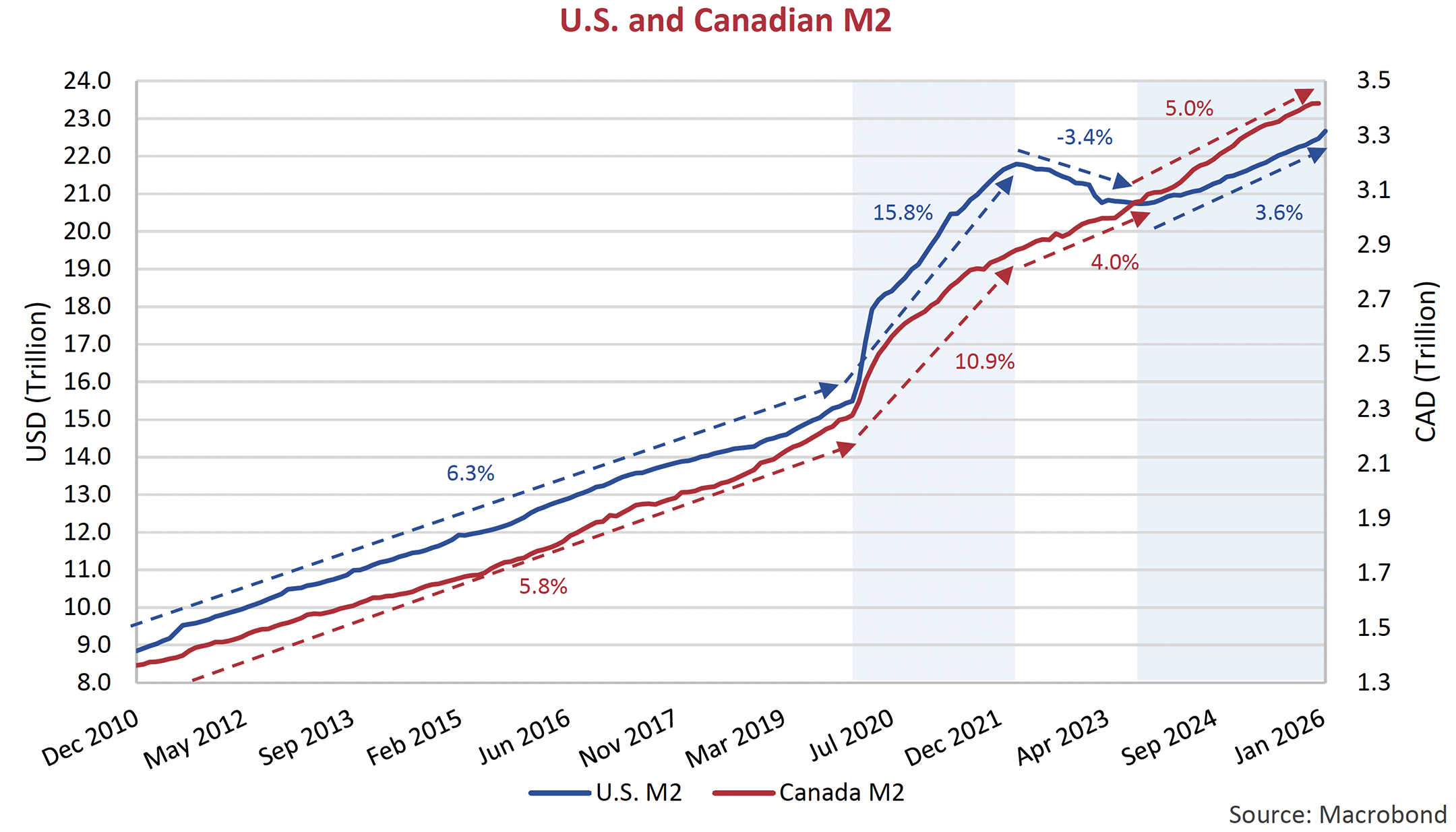

It’s very early in this oil shock, but so far central banks seem to be resisting the urge to ease to help their economies. We think it instructive to look at money supply. The chart below shows the growth in U.S. and Canadian M2 Money Supply. U.S. M2 rose at a 6.3% annualized rate and Canadian M2 rose at a lower 5.8% over the 10 years from December 2010 until just before the pandemic in February 2020. That supported reasonable inflation and economic growth in both economies. Then the Fed, the Bank of Canada and many other global central banks supported their governments’ pandemic fiscal stimulus with the largest monetary ease in a generation. This can be seen in the chart below of U.S. and Canadian M2.

At the outset of the pandemic in February 2020, U.S. M2 was $15.5 trillion. On the back of monetary easing during the pandemic, U.S. M2 exploded to $21.8 trillion in April 2022, a massive 41% in just over 2 years for a 15.8% annualized growth rate. It then fell to $20.7 trillion in October 2023 on tightening monetary policy, a drop of -4.9%, an annualized decline of -3.4% over 18 months. It then returned to expansion at a 3.6% annualized growth to the present $22.7 trillion.

Canadian M2 expanded initially much less over the pandemic, growing from $2.3 to $2.9 trillion, an increase of 10.9% to April 2022. Unlike the U.S. Fed, the Bank of Canada didn’t contract money supply and kept it growing steadily.

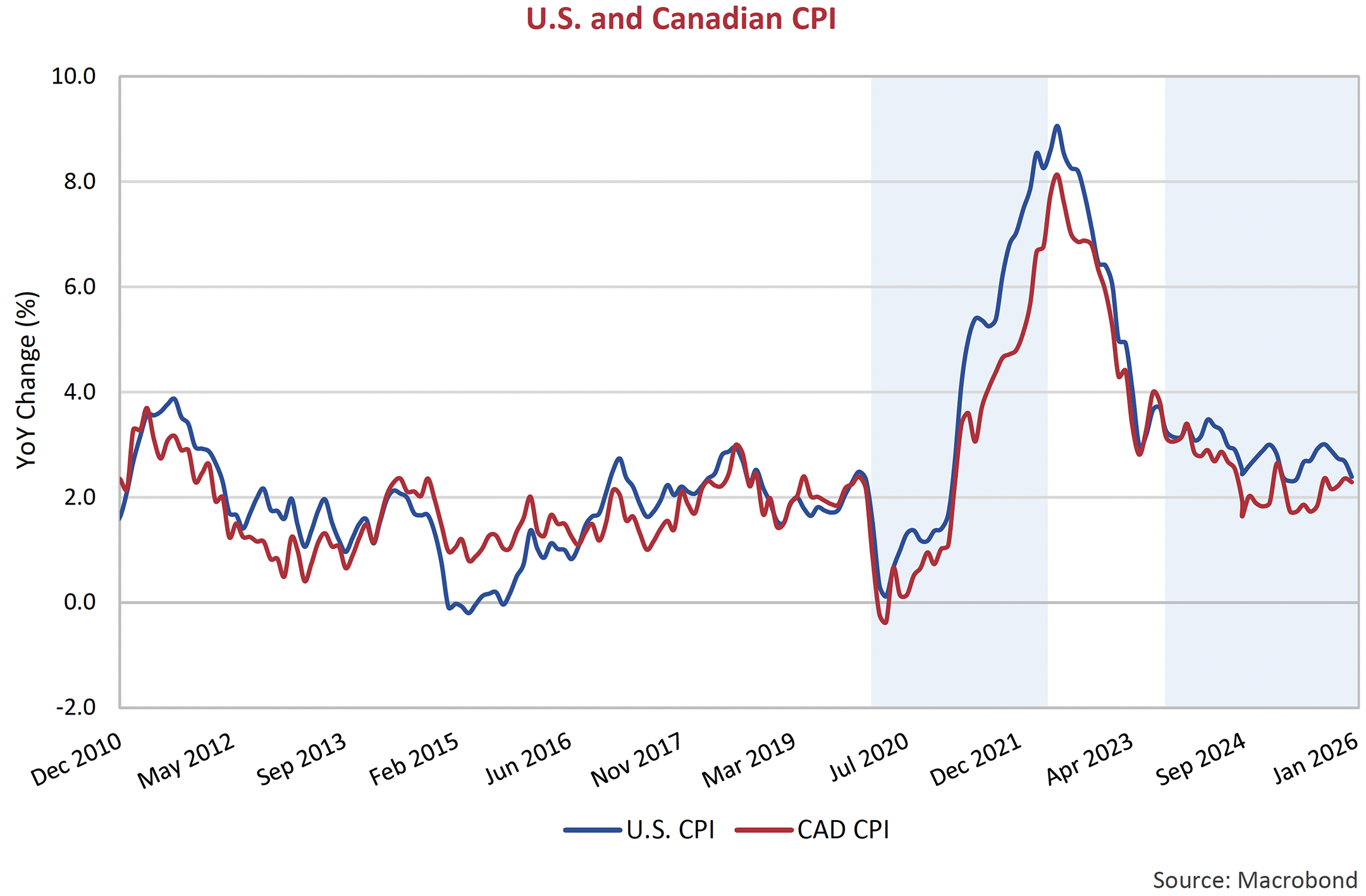

The results of all that money are shown on the chart below of U.S. and Canadian CPI. We have the same periods in blue in both graphs. Note that the period of generationally high inflation coincided with the significant increase in money supply in both countries. Also note that the current moderate growth rates have resulting in moderating inflation. Assuming that our current central bankers have learned this harsh inflation lesson, we are not convinced they will ease excessively for the current energy crisis.

On the other hand, Kevin Warsh, the incoming Fed Chair in May, is replacing current Chair Jerome Powell, who has resisted Trump’s vitriolic demands to ease monetary policy and lower rates. Warsh, given the upcoming October elections, will come under considerable pressure to ease monetary policy to help with this energy crisis. If the other Fed governors don’t agree with looser policy, the Iran crisis just might be accompanied by a Fed crisis!

In conclusion, and as we’ve said previously, expertise doesn’t seem to matter much in Times Trump. Forecasts can be overwhelmed by the mercurial President acting on “gut feel” and few anticipated where the energy prices would be today. We believe that the financial markets are ignoring the scale of disruption in the energy markets, based on investor fears of missing a Trump social media induced rally.

That still has us keeping our portfolios safe in higher quality securities and our few special situations.

Footnotes

- Source: rev. (2026, January 6). Trump speaks after US strikes Venezuela and Captures Maduro.

- Source: Faucon, Benoit. (2026, April 12). The U.S. Sank One of Iran’s Navies. The Other Still Controls Hormuz.

- Source: Leary, Alex. (2026, April 12). Trump Says Oil Prices May Be ‘a Little Bit Higher’

- Source: Reuters. (April 8, 2026). US service sector cools in March; price paid measure highest in 3-1/2 years